In the third quarter of 2024, Flow of Funds data from the Federal Reserve showed that the total value of owner-occupied real estate registered at $48.2 trillion, the second-highest value on record. Despite the ongoing increase in mortgage debt, home equity remained near its peak, holding the second-highest level ever recorded.

Here’s what we learned

The value of homes hits a new high

In 2024Q3, the total value of owner-occupied real estate, the value of all homes owned by those living in them, dropped $0.2 trillion from the previous quarter’s record high, settling at $48.2 trillion. This marks the second-highest total home values on record and reflects a $3 trillion gain over the past year. It is over double the value of real estate 10 years ago when the values were between $20 trillion and $22 trillion, far outpacing the 33% surge in the overall price level per the consumer price index in the past 10 years.

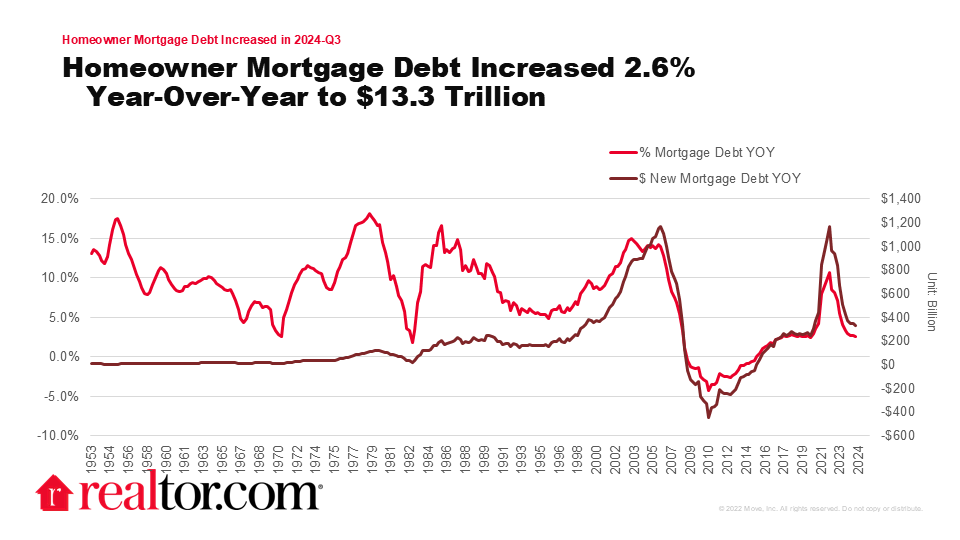

New mortgage debt continued to grow but was issued at a slower pace

During the third quarter of 2024, mortgage debt reached a total of $13.3 trillion, reflecting an increase of $104.9 billion from the previous quarter and $334.6 billion from the same period the previous year. It’s worth noting that this quarter experienced one of the lowest annual growth in household mortgage liabilities, 2.6% year over year, compared with the growth observed between 2020Q3 and 2023Q3. Nevertheless, the annual growth in mortgage debt during 2024Q3 surpassed the range of $237 billion to $276 billion observed between 2017Q3 and 2019Q3.

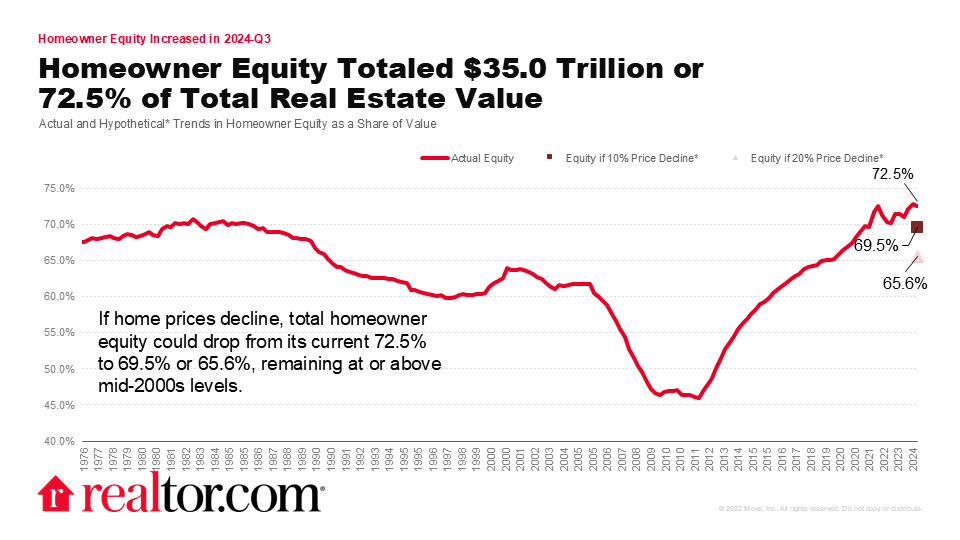

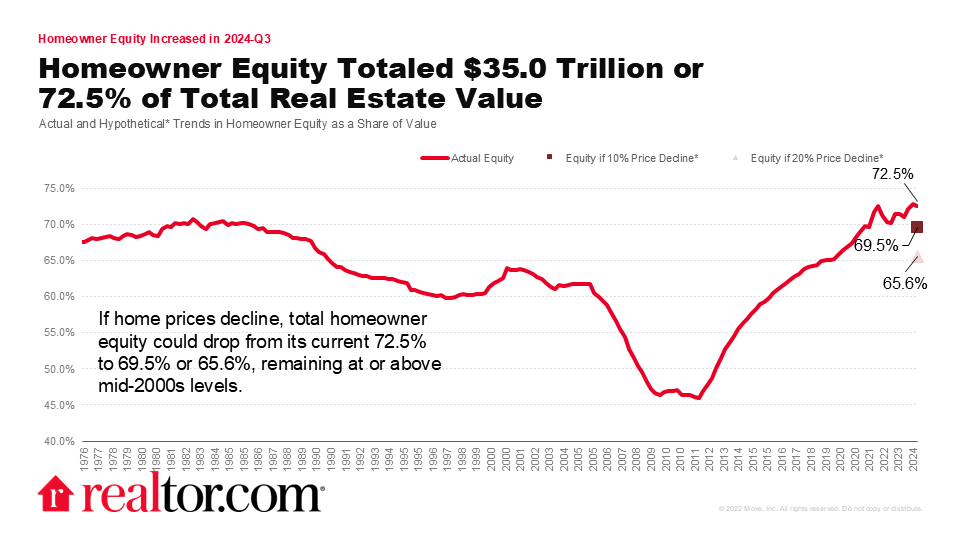

Home equity stays close to the highest level measured

Despite rising mortgage debt, the high real estate values in the third quarter of 2024 allowed homeowners’ equity to remain near record levels. During the third quarter, the total equity held by homeowners in real estate amounted to $35.0 trillion, marking a drop of $0.3 trillion from last quarter but exhibiting a $2.6 trillion increase from the previous year.

Equity, when measured as a proportion of real estate value, is at 72.5%, the second-highest level since 1960. It’s well above the lows seen in 2012 (45.8%) and also above the 60%–65% share it saw through much of the late 1990s and early 2000s. It continues to mark a striking contrast to earlier periods. While concerns persist regarding housing market affordability, it’s evident that today’s households find themselves in a markedly different equity position compared with those in the 2000s.

Home equity continues to be a differentiator in today’s market

Home price declines affect housing equity. Fortunately, today’s high home equity can provide a substantial cushion to existing homeowners in the aggregate. Specifically, the average equity for existing homeowners was roughly around $266,000. Even if the value of homes were to universally decline by 10% overnight from their level at the end of the third quarter, homeowner equity would still be at 69.5%, on par with the second half of 2021. Similarly, a 20% drop in home prices would leave homeowner equity at 65.6%, on par with its level in 2019.

Slow price declines could cause equity to dip further

Even if home prices were to gradually decline over the next two years and mortgage debt continued to rise, homeowners would still have significant equity. This scenario is unlikely, as falling home prices would probably lead to less mortgage lending. However, even under these conditions, homeowners would still have 62% equity in their real estate by the end of that period.

This ending equity result is somewhat lower than what we’d find in the event of an overnight price decline of 20% (65.6%), a reminder of the important role that home lending plays in household equity in real estate, right alongside home prices.

See the full Flow of Funds data.

{kind=link}